Chewy filed an S-1 on April 29th (see filing here). The offering, if executed will be managed by Allen & Company, J.P. Morgan and Morgan Stanley (list in alphabetical order). The company will trade under the CHWY ticker. As yet unclear is which exchange they intend to file on, the amount of proceeds (currently there is a $100 million placeholder, which is standard tactic), or the use of proceeds beyond working capital and general corporate purposes. However, there is much to learn from the filing.

Chewy filed an S-1 on April 29th (see filing here). The offering, if executed will be managed by Allen & Company, J.P. Morgan and Morgan Stanley (list in alphabetical order). The company will trade under the CHWY ticker. As yet unclear is which exchange they intend to file on, the amount of proceeds (currently there is a $100 million placeholder, which is standard tactic), or the use of proceeds beyond working capital and general corporate purposes. However, there is much to learn from the filing.

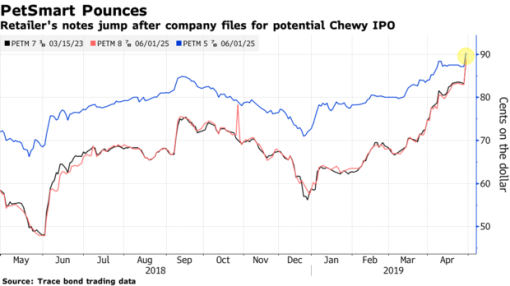

Before wading in, let’s a take a short trip down memory lane. Chewy was acquired by PetSmart for $3 billion in May 2017. As part of a PetSmart refinancing, the buyer borrowed $8.2 billion and the private equity ownership syndicate injected $1.3 billion of equity. The publicly traded component of that debt experienced significant volatility post issuance in-light-of PetSmart’s declining performance. The senior debt tranche traded as low as 70% in May 2018, before rebounding to current levels of 87.5%. The junior tranche traded down to 48%, and today trades at 82.5%, reflecting a much rosier outlook. In June 2018, the ownership group took advantage of an asset stripping clause of the indenture to move 16.5% of the Chewy stock to an unrestricted subsidiary and dividend the parent company 20% of the stock. The value of Chewy at that time was $4.45 billion and notably Chewy will no longer guarantee PetSmart’s debt. Through this process, the equity owners created a war chest that could be monetized to potentially generate a return on their investment or buy themselves out of debt purgatory at a discount. As you might expect, the creditors disputed the parent company’s legality to undertake the asset stripping, questioning whether the business was insolvent. Earlier this month, the two sides agreed to modify the terms of the debt in exchange for dropping the lawsuit. The company’s bond prices spiked upon the announcement of the Chewy S-1 (source: Bloomberg):

Now that we are all on the same page, let’s dig in.

Chewy.com generated $3.5 billion in Net Revenue during 2018, a growth rate of 68%. This figure is slightly more than the estimate category sales on Amazon of $3.3B. Based on the S-1, ecommerce penetration in the category stands at 14%, with growth to 25% in 2022. Notably, Chewy generated a $268 million Net Loss, down from a $338 million Net Loss in 2017. The company warns that profitability may never be achieved, though this is a standard disclaimer. The business currently has 10.6 million customers who order, on average, $334 annually. In 2012, this figure was $223, representing a ~ 7.0% six-year CAGR. Notably, the company states that embedded growth among its customer base is 20%. This is growth that the Chewy would expect to experience through expansion of wallet share if it did not acquire any new customers. Active customers spend, on average $500 in their second year and $750 after their sixth year, 1.5x their second year spend, which is usually their first full year on the platform. The S-1 does not address customer churn. Chewy generates approximately 80% of sales from consumables, of which 5.3% of total Net Sales are attributable to its housebrands.

While all the above is well and good and interesting, the most notable metric is the ratio of customer life-time-value to acquisition-cost, commonly referred to as LTV / CAC. This ratio speaks to how sustainable your customer acquisition engine is and a common predictor of future results. Based on the performance of its 2015 cohort, which is now three years aged, Chewy’s LTV / CAC was 2.4x. The generally accepted benchmark for healthy performance on this metric is 3.0x, indicating some concern with the health of the business model and its ability to become profitable over time.

In thinking about what Chewy might be worth in an IPO, the comp that we gravitate towards is Wayfair. The online retailer of furniture and home goods currently generates $6.8 billion of net sales, losing $404 million of EBITDA. The business currently trades at 2.1x LTM Revenues. When you dig into the comp set analysts rely on in pricing the stock, that group trades at ~ 1.15x Fiscal 2018 Revenue and 1.0x Fiscal 2019 Revenue. This would value the business at $4.1 billion based on 2018 figures and $4.4 billion based on 2019 figures, assuming a 25% growth rate for 2019, with the caveat that no forward guidance is offered in the S-1 but in-line with the June 2018 valuation.

In our Spring Pet Industry report, we postulated that PetSmart may need to sell or IPO Chewy, but the realization of that option is manifesting itself sooner than we had anticipated. The public markets are being tested with offerings of conceptually attractive businesses with a proclivity for losing money. The net of this is the risk reward tradeoff being contemplated here is not without an ample helping of downside potential.

/bryan

Note: This blog is for informational purposes only. The opinions expressed reflect my view as of the publishing date, which are subject to change. While this post utilizes data sources I consider reliable, I cannot guarantee the accuracy of any third party cited herein.

June 13, 2019 at 5:33 am

What’s sad is that Chewy is totally screwing long time employees and anyone not in the C suite by completely redoing everyone’s stock option deals last week. Since the company going public is the 60% Chewy spin off and not the Petsafe-Chewy, everyone is getting a new deal and it’s completely legal. Sumit gets his $17 million dollar payday when he rings the bell and everyone else gets peanuts. Morale is lowest ever. Look for a mass exodus of talent. Look at Glassdoor comments for details.